EOFY cash flow checklist

The end of the financial year is often treated as a reporting deadline. But for many Australian SMEs, it is also a useful time to assess whether the business has enough working capital to support the year ahead.

At Earlypay, we regularly work with businesses that are profitable and growing but still experience cash flow pressure because customer payments arrive after wages, suppliers, fuel, stock and other operating costs are due.

This checklist is designed to help business owners review what cash is coming in, what needs to go out and where pressure could emerge before the new financial year begins.

1. Review what your customers owe you

Start by reviewing your accounts receivable and identifying how much money remains tied up in unpaid invoices.

Check:

- Which invoices are currently overdue

- Whether any invoices are being disputed

- Which customers regularly pay later than agreed

- Whether invoices have been sent to the correct contact

- Which large customer payments are expected in July and August

- How much of your debtor ledger is concentrated among a small number of customers

Use this review to create a realistic collections plan for the first months of the new financial year. It allows you to prioritise overdue or disputed invoices, confirm when large payments are expected and flag any customers whose delays could affect your ability to cover upcoming costs. This gives you a clearer view of whether you need to tighten follow-up, adjust payment expectations or arrange additional working capital before a cash flow gap emerges.

A business can be profitable on paper but still experience cash flow pressure when customers take too long to pay.

For example, a transport business may pay drivers, fuel and subcontractors every week while waiting 30 or 60 days for customers to settle invoices. The work may be profitable, but the delay between completing the job and receiving payment can create a significant working capital gap.

Understanding when outstanding invoices are realistically likely to be paid can provide a more accurate starting point for planning the months ahead.

2. Map your upcoming payments

Create a list of the major payments your business expects to make during the first few months of the new financial year.

These could include:

- Wages

- Superannuation

- Payroll tax

- BAS and tax payments

- Supplier invoices

- Rent and lease payments

- Insurance renewals

- Loan repayments

- Equipment purchases

- Seasonal stock orders

While it’s important to know how much the business needs to pay, it’s just as important to understand when that money will leave the account compared with when customers are expected to pay you.

This can reveal periods when the business may have enough revenue coming in overall but still face a temporary cash flow gap.

3. Prepare for Payday Super

From 1 July 2026, employers will need to pay employees’ superannuation guarantee contributions with each payday rather than following the existing quarterly payment cycle.

For a business with weekly payroll, that could mean moving from four main super payment cycles each year to making super payments each week.

Before the change takes effect, businesses can check:

- Whether their payroll software is ready

- How super payments will be processed

- Whether employee and super fund details are accurate

- How will the more frequent payments affect cash flow

Whether any final obligations from the previous quarterly system remain outstanding

Even where the total annual super expense does not change significantly, paying it more frequently will affect the timing of cash leaving the business.

Businesses should confirm the current requirements with the ATO, their payroll provider or a qualified adviser.

4. Build a cash flow forecast

A cash flow forecast can help a business understand whether it is likely to have enough money available to meet its commitments as they fall due. Cloud-based accounting tools like MYOB and Xero have simple cash flow forecast tools that can be really helpful.

A practical forecast could cover the next 13 weeks and include:

The opening bank balance

- Customer payments expected each week

- Payroll and super payments

- Supplier costs

- Tax obligations

- Rent, finance and insurance payments

- Planned purchases

- Irregular or seasonal expenses

It can also be useful to test a more conservative scenario.

For example, what would happen if several major customers paid two or three weeks later than expected? Would the business still be able to cover wages, suppliers and other operating costs?

Looking at different scenarios can help make potential pressure points more visible before they become urgent.

EOFY is a useful point for business owners to look beyond revenue and profit and focus on timing. A business may have strong sales and a healthy order book, but still come under pressure if wages, suppliers and tax obligations need to be paid before customer invoices are settled. A forward-looking cash flow forecast can help make those timing gaps more visible.

5. Check whether your growth plans are properly funded

Think about what the business hopes to achieve during the new financial year.

Plans might include:

- Taking on a new contract

- Hiring additional employees

- Purchasing more stock

- Upgrading vehicles or machinery

- Expanding into a new location

- Investing in technology

Offering customers longer payment terms

Growth often requires businesses to spend money before the additional revenue arrives.

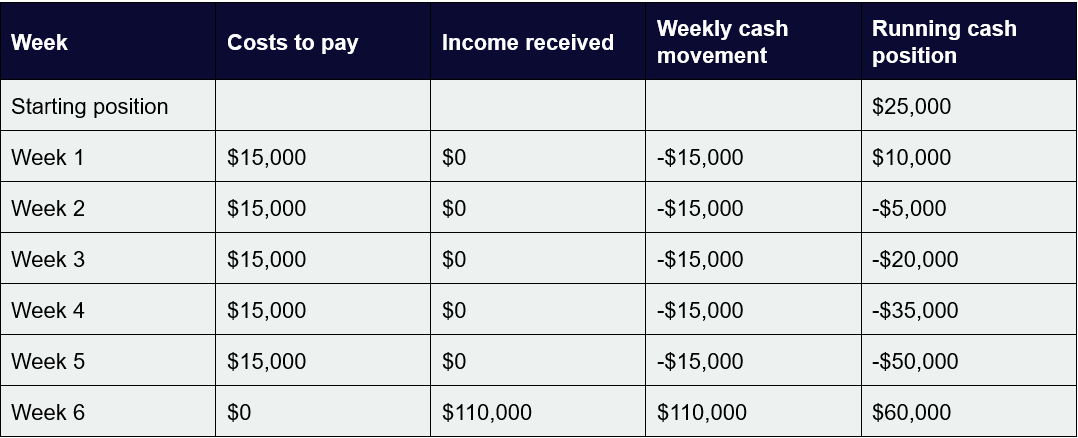

Consider a labour hire business that wins a new contract requiring 15 additional workers. The business may need to fund several weekly payroll cycles, including superannuation, before it receives the first customer payment.

The contract may be commercially attractive, but the business still needs enough working capital to manage the period between paying employees and being paid by the customer.

Estimate the upfront cost of each plan, when the resulting income is likely to arrive and how the gap will be funded.

A simple spreadsheet can help estimate how much cash the business will need before the additional income arrives.

For example:

In this example, the business would need access to at least $50,000 in additional working capital before the first customer payment arrives.

Your plans are only as strong as the cash flow supporting them.

6. Compare customer and supplier payment terms

Review how quickly your business pays its suppliers compared with how long customers take to pay you.

For example, a business may need to pay employees weekly and suppliers within 14 days while waiting 30 or 60 days for customers to settle their invoices. Across a two-month period, that could mean paying money out 8 times, while money only comes in once or twice.

The wider that timing gap becomes, the more working capital the business may need.

Consider:

- The payment terms offered to customers

- How long customers actually take to pay

- The payment terms provided by suppliers

- Whether longer customer terms are affecting the ability to meet other costs

Offering credit terms may help win and retain work, but the effect on cash flow should be understood before committing to them.

7. Review stock, equipment and other assets

EOFY is also an opportunity to look at where cash may be tied up across the business.

Review:

- Slow-moving or obsolete stock

- Inventory levels compared with expected demand

- Equipment or vehicles that are no longer being used

- Assets that may need to be replaced during the coming year

- Maintenance that could prevent more expensive disruption later

- Planned purchases that could be delayed or staged

The $20,000 instant asset write-off has been made permanent from 1 July 2026, giving businesses more certainty when planning future purchases.

Eligible small businesses may be able to claim an immediate tax deduction for the business portion of eligible assets costing less than $20,000, rather than depreciating the asset over a number of years.

However, an immediate deduction does not mean the asset is free or that the business receives the full purchase price back. The business still needs to pay for the asset upfront or arrange suitable finance, so it is important to consider the effect of the purchase on cash flow.

Businesses should check their eligibility and the tax treatment of any planned purchase with their accountant or registered tax agent.

8. Check the true cost of running your business

Costs can increase gradually throughout the year without being fully reflected in a business’s prices or margins.

Compare current expenses with the assumptions used when prices were last reviewed.

Look at costs such as:

- Wages and superannuation

- Materials and stock

- Fuel and freight

- Insurance

- Rent and utilities

- Subcontractors

- Finance costs

- Software and subscriptions

Revenue may have increased while the amount of cash left after operating costs has fallen.

Understanding which products, services or customers are generating sustainable margins can support better planning for the year ahead.

9. Understand upcoming tax and statutory obligations

Review upcoming BAS, tax, payroll tax and superannuation obligations and include them in the cash flow forecast.

It may also help to separate money intended for these obligations from the cash available for everyday business expenses.

Where obligations are already overdue, understanding the total position can help the business discuss its circumstances with its accountant, adviser or the relevant authority.

The earlier a potential shortfall is identified, the more visibility the business has over the options available.

10. Review your existing funding

Consider whether the business’s current funding arrangements remain appropriate for its plans.

Ask:

- Is there enough headroom for seasonal or unexpected costs?

- Does the funding structure match what the money is being used for?

- Could slow customer payments restrict the ability to take on new work?

- Is the business regularly relying on personal funds or credit cards?

- Will upcoming growth create a larger working capital requirement?

- Are existing facilities flexible enough to support changing needs?

Funding is easier to plan when the business has visibility over its future requirements, rather than waiting until a cash flow gap becomes urgent.

Invoice Finance, for example, can allow eligible businesses to access funds tied up in outstanding customer invoices rather than waiting for customers to pay.

The right structure will depend on the business, its plans and the purpose of the funding.

What Earlypay sees in growing businesses

Cash flow pressure is not always a sign that a business is performing poorly.

It can also arise when a business:

- Wins a larger-than-usual contract

- Experiences rapid sales growth

- Needs to fund payroll before receiving customer payments

- Builds stock ahead of a busy period

- Offers longer payment terms to remain competitive

- Invests in equipment before the resulting revenue is generated

- The underlying issue is often timing rather than profitability.

Understanding that timing can help business owners speak more clearly with their accountant, adviser or finance provider about the working capital required to support their plans.

Start the new financial year with greater visibility

Preparing for the new financial year starts with a clear view of the business’s cash flow.

That means understanding:

- What money is expected to come in

- What the business needs to pay

- When those movements will occur

- How late customer payments could affect available cash

- How upcoming plans will be funded

With greater visibility over these areas, you can make more informed decisions about growth, investment and the commitments you take on.

If you invoice other Australian businesses on credit terms, Invoice Finance may provide access to funds tied up in unpaid invoices. This can help eligible businesses manage day-to-day costs or prepare for growth without waiting for customers to pay.

Equipment Finance can also be used for more than purchasing new assets. Businesses may be able to raise capital against assets they already own, providing additional funding for tax debt, working capital, investment or other business needs.

Earlypay has supported Australian businesses with working capital solutions for more than 20 years.

Speak to us about whether our working capital solutions could support your plans for the year ahead.